Why are we integrating with data aggregators?

API-connection improves security, speed, reliability, and visibility

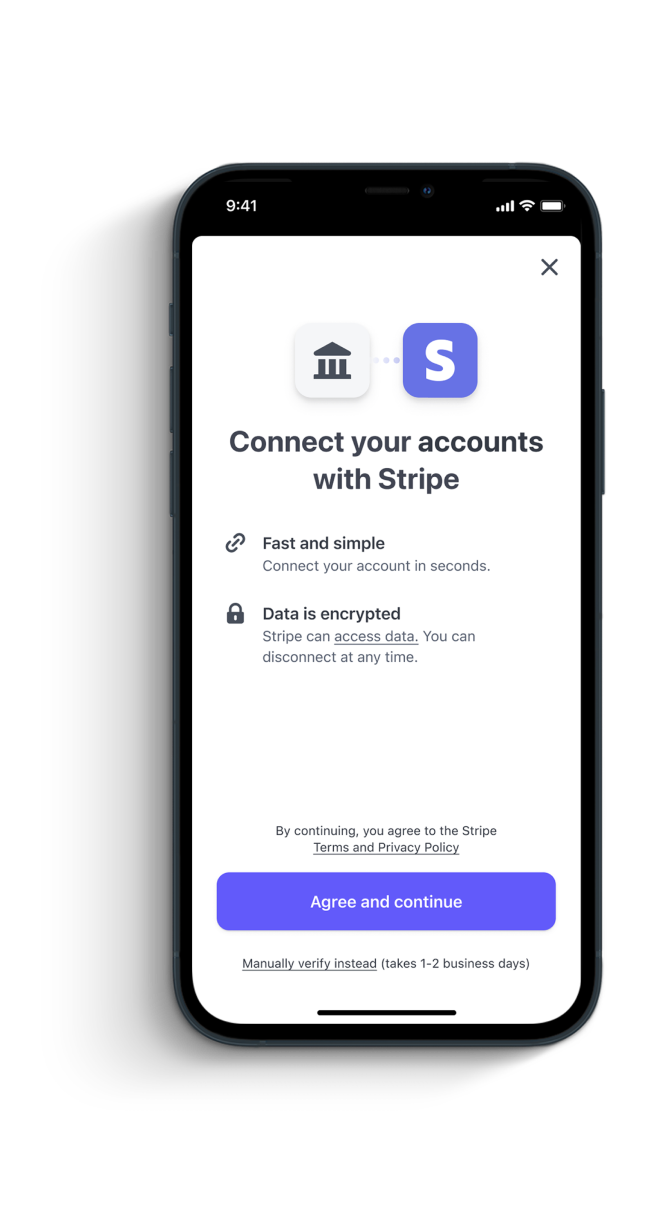

Behavior follows desire. And users want account connection between their financial apps. That's why screen scraping has become so common from services like these data aggregators. The practice of screen scraping by third-party fintechs solved a desire held by accountholders: a way to aggregate specific information from all of their accounts for easier money management. But the practice of screen scraping means handing over your login credentials to a third-party and allowing them to log in on a user's behalf, with no user control over which information is shared. Sound preposterous? It is. And Jack Henry solves this in a better way.

New regulation from the CFPB around screen scraping is being proposed, and many in the industry are hoping for more time to be able to meet new requirements. Jack Henry has known screen scraping to be a security threat for a long time, so we didn't wait for outside regulation to do the right thing and get started solving the problem.

Jack Henry has done the hard work to build partnerships on your behalf with all of the major data exchange platforms. We're proud to say that we've completely replaced in-bound screen-scraping with direct API connection to easily and securely share only relevant data from user accounts to share with third-party fintechs of the user's choice.